If you are an early-stage investor or preparing to secure your second property, you are entering the market at one of the most complex junctures in modern Australian economic history. The property market has hit a massive fork in the road.

Look at the latest data: Commonwealth Bank (CBA) senior economists have downgraded their national housing outlook to a flat 0% growth for 2026. Auction clearance rates have lost momentum, investor sentiment has taken a hit following the Federal Budget’s drastic tax changes, and a stark two-speed market has emerged. While Perth (+1.5% in a single month) and Brisbane (+0.9%) are still moving forward, CoreLogic’s rolling three-month data shows Sydney (-2.1%) and Melbourne (-2.3%) are locked in a clear cyclical downswing.

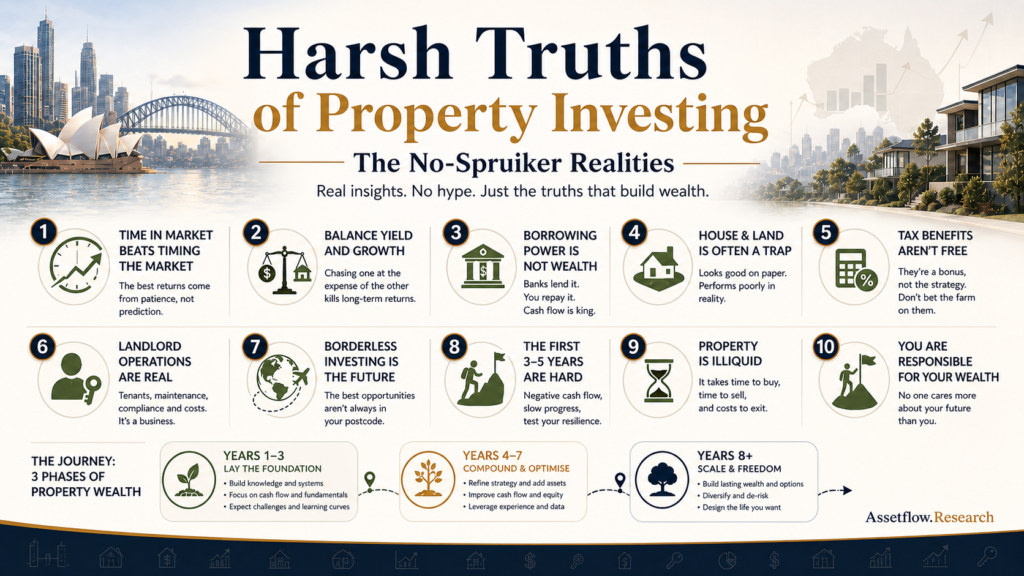

To win in this environment, you have to look past the glossy brochures. Grounded in timeless asset-wealth frameworks and backed by hard numbers, here are the 10 harsh truths about property investing that nobody likes to talk about.

The 10 Harsh Truths

One: You Do Not Make Money on the Purchase, You Make Money Through Time

The media loves a story about overnight equity. The reality, as Stuart Wemyss highlights in Investopoly, is that wealth is a slow, boring compounding process. Real capital growth requires time in the market, not timing the market.

With Sydney and Melbourne values actively sliding from their late-2025 peaks, short-term speculators are panicking. If you aren’t prepared to hold an asset for at least 7 to 10 years to let the land value do the heavy lifting, you are gambling, not investing.

Two: High Yield Won’t Move the Needle, and Pure Growth Will Break You

Chasing pure cash flow (high yield) in isolated regional towns often means sacrificing capital growth, leaving you with an asset that never builds true equity. Conversely, if you chase pure capital growth in premium blue-chip suburbs without a cash flow buffer, current holding costs will force a fire sale.

Ben Kingsley and Bryce Holdaway emphasize in The Armchair Guide to Property Investing that a sustainable portfolio requires a delicate balance of both. Even though combined capital gross yields have ticked up to 3.45%, standard investor mortgage rates are sitting stubbornly above 6.3%. You cannot rely on yield alone to carry a high-growth asset without capital reserves.

Three: Your Borrowing Capacity is Your Absolute Ceiling

Most people think their wealth is limited by how much deposit they can save. It isn’t. It is capped by how much the banks are willing to lend you.

With the RBA keeping the cash rate restrictive, the banking sector’s servicing calculators are punishingly tight. CBA expects new investor lending volumes to halve over the remainder of the year compared to late-2025 levels. Once you hit your borrowing limit, your portfolio stops dead—regardless of how many great deals you find. Managing your borrowing capacity as a finite, precious resource is more important than finding the property itself.

Four: House & Land is a Capital Trap (Unless You Manufacture Scarcity)

Let’s bust a major myth: You can make money on a House & Land (H&L) package during construction. Many buyers have pocketed great equity by the time they got the keys. But here is the harsh caveat—that usually happens because a rising market tide lifted all boats while the bricks were being laid. In a flat 0% growth market like 2026, relying on passive market growth during an 18-month build is a dangerous gamble that often ends in bank valuation shortfalls at settlement. Furthermore, most master-planned estates have zero structural scarcity; you are competing with developers who have five more stages of brand-new land to release right next door.

As Margaret Lomas notes in Investing in the Right Property Now!, you are paying a heavy premium for a depreciating building asset while holding a smaller percentage of land value.

The only way to make H&L win is to step out of the amateur lane. You must target rare, land-locked infill sites where future supply is physically impossible, secure an uncompromised block size, and partner with a top-tier builder under rigid contract terms. If you aren’t doing that level of micro-due diligence, you are buying a marketing package, not a top-performing asset.

Five: Tax Benefits Are the “Icing”, Never the “Cake”

Buying a property specifically to lose money so you can claim a tax deduction is a fundamentally flawed financial strategy. Robert Kiyosaki’s Rich Dad Poor Dad framework reminds us that an investment should ultimately put money into your pocket, not take it out.

CBA’s latest modeling shows that the removal of upfront negative gearing deductions on established properties purchased after 1 July 2027 will strip away roughly $8,600 a year in cash-flow benefits for an investor on the top marginal tax rate buying an $800,000 property. If an asset doesn’t make commercial sense based on local demographics, land scarcity, and organic demand, a disappearing tax credit will not save it from being a dud.

Six: Being a Landlord is an Active Business Operational Game

Property investing is not completely passive wealth creation. It is a business operations game. You will face unexpected maintenance bills, vacancies, and property managers who fail to communicate.

If you treat tenants adversarially instead of treating them as valued customers providing your revenue stream, your vacancy rates will rise and your asset will suffer. As Morgan Housel notes in The Psychology of Money, you must deliberately plan for “room for error”—budgeting a permanent buffer into your ongoing cash flow projections is non-negotiable.

Seven: You Are Competitively Disadvantaged Buying in Your Own Backyard

Human nature makes us want to buy where we live because it feels familiar and safe. But familiarity is not a data-led investment strategy.

If you live in Sydney or Melbourne where prices are undergoing an orderly decline, forcing a purchase locally just out of comfort means you are likely buying a compromised asset (like a high-density unit) to fit your budget. Canstar modeling recently warned that a Melbourne first-home buyer with a 5% deposit could easily owe more than their home is worth by December. To win, you must develop a borderless mindset and deploy your capital into markets where the data—not your emotions—indicates outperformance.

Eight: The First 3–5 Years of a Portfolio Usually Feel Horrible

Steve McKnight hints at this in his foundational writings: the start of the journey is an uphill battle. When you buy your first one or two properties, your cash flow is stretched, mortgage payments feel heavy, equity growth looks agonizingly slow on paper, and every repair bill causes micro-panic.

It takes time for inflation to erode the real value of your debt and for organic market rents to rise enough to create a comfortable cash-flow cushion. You have to survive the stressful “infancy phase” of a portfolio before you get to enjoy the fruits of a mature asset base.

Nine: Property is Incredibly Illiquid—Getting Out Costs a Fortune

Unlike shares, where you can liquidate your position in seconds for a small brokerage fee, property traps your capital. If you buy the wrong asset and need to exit, you will lose roughly 5% to 7% of the property’s value instantly to agent fees, marketing campaigns, settlement costs, and capital gains tax. If you make a bad purchasing decision today, turning around and selling it can set your financial timeline back by half a decade.

Ten: No One Cares About Your Wealth More Than You Do

The property industry is flooded with players who make money from the transaction, not the long-term performance of the asset. Real estate agents represent the vendor, mortgage brokers get paid on loan volume, and developers need to clear their balance sheets.

If you outsource your thinking entirely to a third party without understanding the data yourself, you are flying blind. As a mentor, my job is to teach you how to read the data from CoreLogic, SQM, and the ABS so you can make your own calculated, independent decisions.

Cut Through the Noise: The 3-Step Action Plan

To help you digest these truths and see how they interplay over time, look at this lifecycle framework:

[ Phase 1: Years 1-3 ] --------> [ Phase 2: Years 4-7 ] --------> [ Phase 3: Years 8+ ]

- Cash flow is tight - Rents rise organically - Equity compounds

- Portfolio infancy - Debt value erodes - Unlocked buffers

- Surviving the "Noise" - Stability achieved - True wealth phase

If you want to cut through the current media storm and take an active, confident step forward within the next two to three weeks, follow this exact checklist:

Step 1: Lock in Your Absolute Financial Truth (Days 1–5)

Stop guessing what you can afford based on online calculators. Schedule an urgent strategy session with an investment-focused mortgage broker. Establish your precise borrowing ceiling under current servicing guidelines, calculate your actual out-of-pocket holding costs at current interest rates, and determine your available cash buffer.

Step 2: Draw Your Line in the Sand (Days 6–10)

Based on your budget, choose your strategy. Do not try to look at everything at once.

- If your budget is under $600,000: Turn your focus entirely toward affordable capital city rings or strong regional hubs where you can still secure a freestanding house on a decent block of land with a vacancy rate well below 1.5%.

- If your budget is over $800,000: Focus on the cooling major capitals where stock is building. Identify A-grade, established properties (such as mid-century brick units or houses in tightly held inner-ring suburbs) where vendor expectations have softened, and prepare to negotiate.

Step 3: Run the Numbers on 5 Real Opportunities (Days 11–15)

Select one targeted location that hits your brief. Find five properties currently on the market and run a brutal analysis on each. Check the suburb-level vacancy rate on SQM Research (if it’s above 2%, scratch it off), compare the asking price against recent comparable sales via CoreLogic data, and calculate the land component value. Pick the top two properties from your list, call the listing agents, and find out the vendor’s true motivation.

The Next Step: Build Your Bulletproof Property Blueprint

The 2026 property market isn’t broken—it’s just unforgiving to amateurs. The upcoming 13-month grandfathering window before the Federal Budget’s tax changes kick in represents one of the final opportunities to build a portfolio under the old, highly advantageous rules. But you cannot afford to execute with a flawed strategy.

At Asset Flow, I don’t sell property, and we don’t take kickbacks from developers.I build property strategists.

If you are ready to stop letting headline noise dictate your financial future, let’s look at your personal numbers, map out your borrowing capacity, and identify the exact markets that fit your wealth goals.

Disclaimer: This article provides general information and educational commentary only. It does not constitute personal financial or investment advice. Before making any property investment decisions, you should seek independent financial, legal, and taxation advice tailored to your individual circumstances.