1. Personal Analysis: The Great Rate Myth vs. The Market Reality (2010–2026)

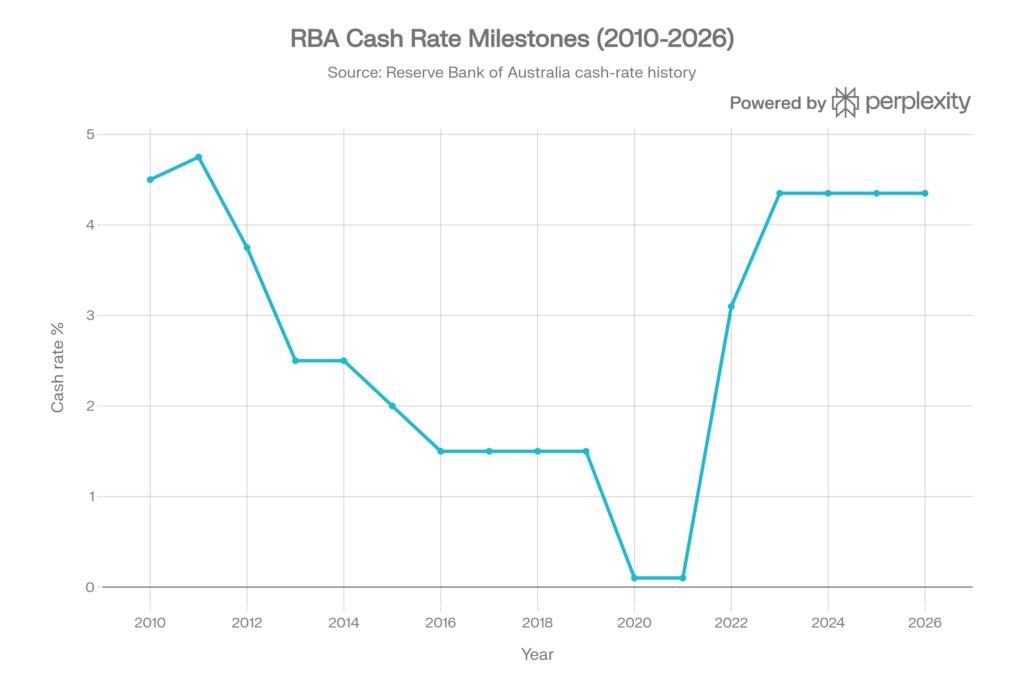

Last week, the RBA handed down its third interest rate hike of 2026, pushing the cash rate to 4.35%. While the headlines are screaming “downturn,” I spent some time mapping out the RBA cash rate against capital city median prices from 2010 to today. The results confirmed a hard truth: The rate hike is a headline, but supply is the trend.

📊 Data Analysis: RBA Cash Rate vs. Capital City Medians

| Year | RBA Cash Rate | Sydney Median | Melbourne Median | Brisbane Median | Perth Median | The Market Context |

| 2010 | 4.50% | ~$600k | ~$500k | ~$450k | ~$480k | Rates were higher then than they are today. |

| 2016 | 1.50% | ~$1.1M | ~$800k | ~$550k | ~$500k | Cheap money fueled the East Coast surge. |

| 2020 | 0.10% | ~$1.2M | ~$900k | ~$650k | ~$480k | The “Emergency Low” that sparked the boom. |

| 2022 | 3.10% | ~$1.4M | ~$1.05M | ~$850k | ~$600k | The Hike Shock: Rates jumped from 0.1% to 3.1%. |

| 2024 | 4.35% | ~$1.6M | ~$1.05M | ~$1.05M | ~$850k | The Resilience: Prices climbed despite 13 hikes. |

| 2026 (Now) | 4.35% | ~$1.7M | ~$1.2M | ~$1.2M | $1.1M+ | The Supply Paradox: New record highs nationwide. |

My Key Takeaways:

- The “Wait and See” Trap: In 2010, the cash rate was higher than today (4.50%) and Sydney’s median was $600k. If you waited for the “emergency low” rates of 2020, you ended up paying double. You “saved” on interest but lost $600k in equity.

- The Supply Paradox: Despite rates hitting 4.35% again, the National Shortfall (approx. 300,000 homes) is keeping a floor under prices. In high-demand micro-markets like Perth and Brisbane, the inventory is so low that prices are still climbing regardless of the RBA.

If the math works today, it’s a “Yes.” Hoping for “cheaper” next month isn’t a strategy; it’s a gamble.

2. The Insider Scoop: Orchestrated Expert Consensus

To build a portfolio in 2026, you have to move past “General News” and look at the Inventory Heat Map—the lead indicator that tells us where prices are headed before they move.

- The “Months of Stock” Indicator: I follow the speed at which the market “consumes” houses. We calculate this by taking Total Active Listings and dividing them by Average Monthly Sales.

- > 6 Months: A Buyer’s Market (negotiate hard).

- < 2 Months: An Extreme Seller’s Market (The Pressure Cooker).

- Current Pulse: While Sydney has loosened slightly, markets in Perth and Brisbane are currently sitting at less than 1.5 months of stock. When supply is this thin, price growth is a mathematical certainty. In one of my next posts, I would write about how using Perth and Brisbane as umbrella stats might also be counterintuitive.

- The “Equity-First” Pivot: Experts agree that waiting for a 0.25% rate cut is a wealth-killer if the market moves 7% in that same year. The “Smart Money” is accelerating searches now to beat the next growth cycle.

- The “Serviceability” Self-Sustenance: In a 4.35% environment, assets must be Self-Sustaining Systems. We are prioritizing properties that “pay their way” from day one to ensure your borrowing capacity remains intact for the next move.

- The Budget “Policy Window”: The consensus is that major tax shifts (like CGT or Negative Gearing) rarely happen overnight. The expert advice isn’t to “panic-buy” by Tuesday; it’s to accelerate your planning. Be “in the system” before new rules are legislated to ensure maximum adaptation time.

3. The Pulse: Top 3 Trends (Early May 2026)

- The “May 12” Speculation (Search Volume +350%): Google Trends shows a breakout in searches for “Grandfathering Negative Gearing.” Investors are finalising due diligence and getting “offer-ready” to secure current tax treatment before the Federal Budget on Tuesday.

- The “Established Land” Premium: Due to high-profile builder insolvencies, search interest for “1950s/60s Established Homes” has surged by 72%. Buyers are prioritizing “Intrinsic Value”—the security of a home already standing on a solid block—over construction risk.

- The “Migration Pivot” (The Rent-Shield Strategy): Families are moving from renting in hubs like Parramatta to buy in corridors like Schofields or Marsden Park. They are buying for three reasons:

- The “Inflationary Rent” Trap: Rent is a variable cost (rising ~10% annually). A mortgage is “locked” against your purchase price.

- The Equity Dead-End: Rent is a 100% loss in cases when you are paying it week on week without a clear Rent-Vesting strategy. Moving to an outer-ring growth corridor allows you to build an asset that historically grows.

- The “Crossover” Logic: We are mapping the point where mortgage repayments become cheaper than rent. In growth zones, this is accelerating. You trade short-term “repayment pain” for a lifetime of asset control.

4. Your 14-Day Action Plan: The Acceleration Phase

- Days 1–7: Perform a “Budget Exposure” Audit. You don’t need to panic-buy this weekend, but you do need to know where you stand. Sit down with your broker and accountant to model your current holdings against the rumoured shifts. Having these scenarios modeled before Tuesday night allows you to accelerate your decision-making once the actual papers are released.

- Days 8–14: Audit your “Commute Ceiling” and the Pipeline. If you are in the market for a PPOR and considering the Migration Pivot, look beyond the house. Research the Infrastructure Pipeline—specifically the 2-year and 5-year plans for road widenings (like Richmond Road in Western Sydney) and rail extensions. Ensure the government’s spending plan is actually working to eventually give your commute time back to you.

What I can offer:

I’ve lived through the anxiety of renting out my first home and the stress of buying a 1957 “time capsule” while the world was locking down. To help you accelerate your approach—strategically, not frantically—I am offering a limited number of Mindset Review Sessions this month. Comment below and let me know if you would like to enrol…

In this session, we will:

- De-code the “Rate Rise Fear” vs. the cold, hard supply-demand data.

- Shift your lens from “Home” to “Asset” to ensure your next move protects your future borrowing capacity.

- Audit your “Support Squad” to ensure you have the right architects in your corner to navigate the post-Budget landscape.